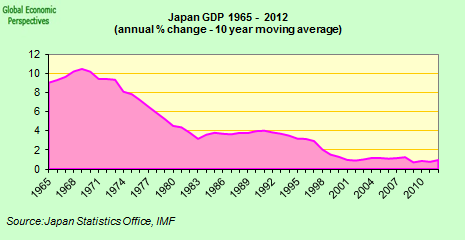

I've been pretty quiet on Japan recently. This is because I think we need to wait and see what kind of reality there is behind the optimistic projections - and share prices - that we have been seeing recently. I don't think the problem, has gone away by any means. At best we are on the upswing of what remains of the business cycle in Japan. The economist is not too convinced either, and has coined the expression 'dysflation' for the Japanese condition. What I still think is unfortunate is that virtually no-one is prepared to even countenance the idea that Japan's demographic problems (and it's resistance to immigration) could have any part in the explanation. The idea isn't even examined in order to discard it. It seems to be a blind spot pure and simple.

So what exactly ails Japan? Clearly not just the usual sort of business downturn, which can be cured, though painfully, with lay-offs and closures and sometimes with a government shot in the arm. Nor can its chronic weakness be attributed solely to a burst bubble and falling asset prices, though that is clearly part of the problem. Many other countries have been similarly stricken, and have managed to recover. In Japan, the misery has lasted for almost 14 years.

The Economist would like to suggest its own label for Japan's illness. It is �dysflation�: a form of deflation in which dysfunctional economic-policy institutions counteract what would otherwise be good medicine for falling prices. The policies, especially with regard to banks, combine in ways that do more harm than good. More important, policymakers themselves are more inclined to avoid problems than address them; would rather win bureaucratic feuds than co-operate; and base most of their decisions on emotion (such as fear of shame) rather than reason.

It helps to keep all these aspects of dysflation in mind when assessing Japan's problems. Consider, for example, the Bank of Japan. Ordinarily, the best response to deflation�that is, falling prices throughout the economy, and not merely for a few products such as Chinese manufactures�would be lower interest rates and feverish printing of money. Japan has had zero interest rates since 1999, however, and has been boosting the money supply at a rapid clip since early 2001�and prices have continued to fall. According to the most respectable measure, the GDP deflator, they have fallen 7.6% since 1997, and are still dropping fast. Eventually, all the money that the Bank has been printing will be sucked through the financial system and expelled into the economy in the form of higher prices and rising nominal interest rates. But it is taking a perplexingly long time to happen.

The Bank's explanation is that Japan's deflation is a very rare strain indeed. It points to the large quantity of non-performing loans that have piled up in the banking system. Never in the history of human endeavour have so many owed so much for so long. And as the Bank's officials like to point out, new bad loans, at least until recently, continued to accumulate faster than the banks were writing off old ones, and the Financial Services Agency (FSA), which regulates banks, has done nothing to stop this. Banks are lending mainly to their worst borrowers; and with the credit channel not operating properly, the usual monetary-transmission mechanism cannot work either.

There is probably some truth in this argument. What it ignores, however, is the overarching role that expectations�of firms, workers, consumers and investors�play in transmitting the central bank's policies into rising or falling prices, and the need for the central bank to manage those forecasts. The Bank has not only failed utterly in this role, but has refused to take responsibility for trying.

Under the previous governor, Masaru Hayami, whose term began in 1998, every constructive policy that the Bank undertook was undermined by a statement that the Bank did not really expect its policy to get prices rising again, at least not quickly. This had a sort of reverse placebo effect. Even as the central bank was administering potent medicine, Mr Hayami said that it was only doling out sugar cubes. A new governor, Toshihiko Fukui, took over in March, and has been an improvement. Conceivably he will do a better job than Mr Hayami of convincing people that all that loose money will not be vacuumed up again at some point by the Bank. But even Mr Fukui has shown traces of his predecessor's dysfunctional approach.

Source: The Economist

LINK