---

We are now ready to another trip around the economic commentaries dealing with the Japanese economy and its sustainable/ongoing recovery. For a list of my recent post on Japan go here.

Let us begin with the those who are getting it right. First off, the FT's Lex column seems to be on the right track concerning Japan. Back in September Lex ran a column asking about what in fact was happening to the Japanese recovery based on disappointing data coming out from June. This week Lex also takes on Japan in one of her columns pointing once again to weak data especially on lending and subsequent consumer spending.

(bold parts are my emphasis in terms of all excerpts presented below)

What recovery? Japanese economic data continue to disappoint. The latest, published on Thursday, show bank lending growth decelerated on an annualised basis in October, for the third month in a row. City banks actually lent less than a year ago.

Borrowers are clearly in short supply. Companies are less willing to invest. Even if they were willing, most have plenty of cash on their balance sheets. Nor is it just borrowers who are thin on the ground. Shoppers too are holding back, as the government knows to its cost: consumption tax revenues fell 3 per cent year-on-year in the six months to September. Private sector economists are slashing estimates for third-quarter growth, due out on Tuesday. Since consumption alone fell 0.9 per cent, it is possible the economy contracted.

Also the FT's David Pilling is scratching the right places in an article discussing how the BOJ might act pre-emptively against inflation and raise rates come next meeting (that is, some time before the end of the year). Yet as Pilling so rightly points to (at least implicitly); what inflation? If we discount the headline Japan is still running deflation and even including energy Japan is flirting with a potential backlash into a vicious deflationary circle.

Speaking to a seminar in Tokyo, Mr Fukui said: “Waiting for inflation to build up in raising interest rates would cause a sharp swing in the economy. Our task is … to take careful action before these conditions appear in order to achieve price stability and keep future economic swings gradual.”

The governor’s comments come against a background of weak headline inflation and concern among some analysts that the economy, which is going through a weak patch, could actually slip back into deflation.

His remarks reinforce the bank’s insistence that it will not tie its policy to the headline rate of inflation, which has been sliding, partly due to technical factors.

Instead, the BoJ, which raised rates in July for the first time in six years to 0.25 per cent, wants room to be able to act against inflationary pressures before they are apparent. It has what some economists consider to be an overly conservative understanding that price stability equates to an inflation rate of between zero and 2 per cent.

This allows no buffer against slipping back into deflation, and the bank has resisted hitching its policy to a specific inflation target.

Jonathan Allum, Japan strategist at KBC Financial Products, said: “The nightmare scenario is that A: you begin to see evidence of economic contraction, B: you get a return to deflation, and C: the Bank of Japan ignores all this and tightens anyway.”

Mr Allum said the economy had been slowing for nearly a year and that it could even contract in the third quarter because of sluggish consumer spending. “Clearly there is a danger that the BoJ is too gung-ho in its view of the economy,” he said. “If energy prices are excluded, as they are in most economies, Japan is still in deflation.”

So these were the ones getting it right. Moving on I should say that I do not have an FT subscription but instead I have chosen some three years ago to go with The Economist. I stand by that decision but in no way because of the magazine's continuing la-la position on Japan. Consequently, The Economist runs a story this week about the 'vigorous' state of the Japanese economy.

The school of Japan-watchers that keeps an eye on the country's economy chiefly out of a morbid interest in terminal decline (ouch :)) has stopped dwindling . It has even taken on new adherents of late. For signs are mounting that the recovery that began in 2002 has slowed—or even, some say, gone into reverse.

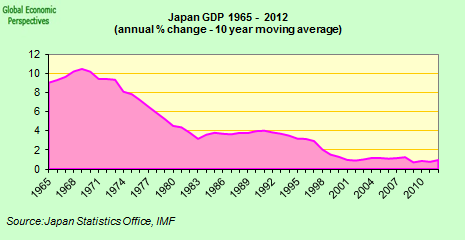

The chief worry is that what started as a recovery driven by exports (chiefly to China), and then expanded to one led by business investment, has failed to spread to households, whose spending remains sluggish. Prices still flirt with deflation (see chart). And some economists predict that figures published on November 14th will show that the economy actually shrank in the third quarter.

Is this growing uneasiness justified? Mostly not. Take the economy first. Certainly, its anaemic performance marks this recovery as out of the ordinary, but then it follows long years of extraordinary distress. Habits are hard to change. So even though households now have more income—because companies are hiring more, and raising overtime and bonuses—this has not shown up in consumer spending. Alarm mounted last week when the main survey of household spending recorded a plunge in September of more than 6% compared with a year earlier. Yet this fall is too big to be credible; the survey (like early GDP numbers and other Japanese statistics) is notoriously unreliable.

Meanwhile, expectations are rising, even if habits have not yet caught up. Households' estimates of future inflation and property prices have climbed since the spring. People are not spending gaily, but they are starting to remove money from risk-free havens and invest it again. Deflation had killed the appetite for risk. There are other signs that the recovery is still broadly on track, even if it has, as in 2004, hit a soft patch. The latest bank lending figures seem to confirm this: though growth slowed in October, the year-old recovery in bank lending is still intact.

(...)

Moving forward in Japan? Well, certainly and good all the same! Addressing the Japanese 'dual-economy.'

A priority is to address Japan's so-called “dual” economy. The competitive exporting industries are not matched in agriculture and services, which are shielded from competition, lack economies of scale and are backward in their use of information technology. To boost investment, the government is mulling a cut in corporate income tax and other tax changes. Deep reforms to pensions and health care are also expected.

oh yes, and to use a classic proverb - it's the demographics stupid!

Japan's demography, says Genichiro Sata, the minister for regulatory reform, demands higher growth, and it is the Abe government's intention to impart deep structural change—including even a wholesale restructuring of government, by crunching Japan's 47 prefectures into a handful of American-style states. These are early days. Mr Abe has given little sense yet of his priorities, and many of the proposals are hardly vote-winners. Reformist achievements are yet to be seen. But the charge that Mr Abe has no reformist intentions is getting harder to make.

Ok, am I being too much of a dooms-speaker here on Japan? Perhaps I am but only time will tell really. What I would like to do though is to make a point across the table here. Japan as a society and in this case as an economy is deeply affected by its demographics, subsequent low fertility and more importantly high median age. Demographics are not destiny but if we begin here I feel that much of Japan's current economic plight can be explained in its core. As such, I believe that the continuing lack of consumer spending is not subject to an automatic reversal as The Economist rather naively, I am sad to say, suggests. In fact, low consumer spending is a structural indicator of Japan’s population structure which is also why Japan is running a trade surplus and also why in the end Japanese economic growth is by and large export driven. I hardly think it is a problem of ‘habits which merely take time to adjust.’ This argument has wide consequences for the way we look at Japan and its problem with deflation which after all must also be considered a structural phenomenon in the economy. Even more obvious is the labour supply where many a commentator (although not any linked here!) have argued that the tightening labour market was a cyclical phenomenon pointing to supply having problem keeping up with demand as the recovery really got underway. I am sympathetic to this point since it is theoretically a good point, just not in Japan where the age composition of society is a proxy for tightening of the labour supply and as such is a structural effect of the changing pyramid more than a cyclical fluctuation.

So let us begin with a strong basis of analysis and move our way up from there, that is really all I am pointing to.

---

And the Update 11 November based on the latest data on machine orders.

Sadly the data keeps on going the wrong way for Japan.

(From Bloomberg - bold parts are my emphasis)

Japanese machinery orders unexpectedly slumped, signaling economic growth may stall and prevent the central bank from raising interest rates, already the lowest among major economies. Stocks fell.

Non-government machinery orders, excluding shipping and utilities, dropped a seasonally adjusted 7.4 percent to 997.5 billion yen ($8.5 billion) in September from a month earlier, the Cabinet Office said in Tokyo today. Third-quarter orders sank 11.1 percent, the biggest decline ever.

Bonds rose on expectations that the report, an indicator of capital spending plans, will ease the Bank of Japan's concern its key overnight lending rate of 0.25 percent could fuel excessive investment. Next week's gross domestic product report is expected to show corporate spending growth slowed in the third quarter.

`The drop in machinery orders was a surprise,'' said Soichiro Kimura, an analyst at Mizuho Securities Co. in Tokyo. ``It's adding to speculation the report will weaken the central bank's case for raising rates.'' `

(...)

``The gap between the actual economy and the Bank of Japan's view might be widening,'' said Hiromichi Shirakawa, chief economist at Credit Suisse Group in Tokyo.

Sustained growth in exports, the only standout in the quarter, will be key in ensuring business investment keeps rising, Dai-Ichi's Iizuka said.