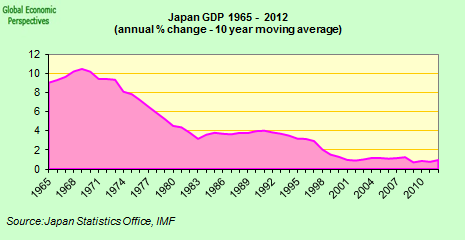

It has been a while since I have last reported on Japan and I even manged to slip on the Q1 GDP figures which showed in unconventional fashion how consumer spending acted as a cushion for declining industrial production. As such, here is a short note which should bring you up to date with the latest ...

On the Q1 GDP figures they should of course to be taken with a pinch of salt since the Japanese trade surplus widened all through Q1 on strong demand from Europe and the rest of Asia (China) even as exports expectedly slowed slightly to the US on the back of sluggish performance in the first quarter. So, capex cannot continue to slump forever in Japan if the trade surplus keeps widening and at some point those inventories although very full from Q4 06 will be depleted. Edward Hugh has an excellent round-up of the recent data and commentary coming out of Japan surronding the first quarter data releases.

Now, the recent data from Japan is indeed interesting and whilst Edward is covering the dip in unemployment from 4% to 3.8% noting the interesting point that wages still are stubbornly reluctant to rise (where is that damn NAIRU? :)) I am going to treat the figures for consumption expenditure which show a y-o-y increase of 1.1% in domestic consumption. As such, we need, as ever I guess, to dig a bit deeper than the traditional (although much appreciated) Bloomberg headline of 'an unexpected accelaration ...'

The immediate point I think should be noted is the nature of the main figures provided by Bloomberg and thus the Japanese statistical offices which are not seasonally adjusted. This is of course not a major issue but the difference revealed in these two figures is fairly large and generally there is much more in the Japanese consumption figures than the headline increase of 1.1% (in this concrete case) would lead you to believe. First of all, we can of coure try to even the average monthly increase in y-o-y consumption expenditures (see here) which amounts to an average increase of 0.8%. This is of course not an outright decline but still hardly sizzling either. Moreover, if we break down the headline figure into sub components we see that education accounted for a above average part of the increase. This coupled with household equipment and medical care were largely what drove the increase in consumption expenditures in April, and we need to ask ourselves whether for example the sub-component 'education' will continue to expand at this pace although of course other sub-components might take over (recreation and culture for example?). The last thing of note is that retail sales continued a six month decline according to Bloomberg although they also make a point on noting that retail sales figures should be taken with a pinch of salt since they do not take into account all those internet savy Japanese consumers buying goods over the internet.

Update

A couple of addendums ...

Surprisingly, industrial production slipped again in April which indeed does seem odd given the fact that the trade surplus seems to be widening.

Japan's industrial production unexpectedly fell for a second month in April as the slowest economic growth in the U.S. in four years reduced demand for Toyota Motor Corp. and Honda Motor Co. cars.

Production slipped a seasonally adjusted 0.1 percent after declining 0.3 percent a month earlier, the Ministry of Economy, Trade and Industry said in Tokyo today. The median estimate of 46 economists was for a 0.5 percent increase.

Also, wages slipped again in April which of course does not bode well for the future of domestic demand in Japan.

Japan's wages unexpectedly fell for a fifth month, hampering a recovery in consumer spending that's being fueled by job growth.

Monthly wages, including overtime and bonuses, declined 0.7 percent in April from a year earlier, the Labor Ministry said today in Tokyo. The median estimate of eight economists surveyed by Bloomberg News was for a 0.1 percent increase.