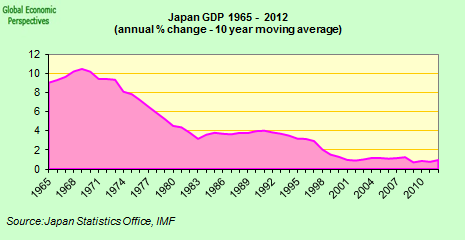

If you have been following my notes on Japan's economy you might have noticed that the measures of inflation represent something of a maze. Basically, I usually cite three measures of inflation in ny notes on Japan as can be seen from the graph below from one of my recenc posts ...

Regarding the official data which comes out of the Japanese statistical office and which is subsequently cited by Bloomberg, Reuters etc we are looking at the green line which measures the general index less fresh food. This also means that the official Japanese inflation measure includes headline inflation represented by energy prices. Now, the measure of inflation in Japan is of course far from trivial since in an economy cruising very close to deflation the central bank and thus markets are using even small fluctuations in prices as a base for migthy important and far reaching decisions. But what prices should we be looking at and is Japan currently in deflation or inflation? Regarding the former this is set, I think, to hit headlines very soon as it seems as if structural inflation pressures are set to mount. Remember here that while the recent surveys indeed show that inflation expectations are rising in Japan much of this is due to a perky headline. As such, there is a risk that inflation measures in Japan might very well diverge in the coming months something which could indeed help the BOJ but if domestic demand does not follow back up then of course the BOJ will be stuck between a rock and a hard place.

Turning to the latter and whether Japan is in fact in deflation or inflation and how gauge this we move to the real impetus for this entry. In this way Christian Broda and David E. Weinstein recently had a paper published at the NBER on price stability in Japan which highlights some of the important issues with the measurement of Japan's inflation rates. Now, if we disregard the implicit narrative (true as it may be) that US methodology is superior I think that there are some important points most notably of course the general point about how Japan's inflation index is biased upwards. Here is the abstract ...

Japanese monetary and fiscal policy uses the consumer price index as a metric for price stability. Despite a major effort to improve the index, the Japanese methodology of calculating the CPI seems to have a large number of deficiencies. Little attention is paid in Japan to substitution biases and quality upgrading. This implies that important methodological differences have emerged between the U.S. and Japan since the U.S. started to correct for these biases in 1999. We estimate that using the new corrected U.S. methodology, Japan's deflation averaged 1.2 percent per year since 1999. This is more than twice the deflation suggested by Japanese national statistics. Ignoring these methodological differences misleading suggests that American real per capita consumption growth has been growing at a rate that is almost 2 percentage points higher than that of Japan between 1999 and 2006. When a common methodology is used Japan's growth has been much closer to that of the U.S. over this period. Moreover, we estimate that the bias of the Japanese CPI relative to a true cost-of-living index is around 2 percent per year. This overstatement in the Japanese CPI in combination with Japan's low inflation rate is likely to cost the government over 69 trillion yen -- or 14 percent of GDP -- over the next 10 years in increased social security expenses and debt service. For monetary policy, the overstatement of inflation suggests that if the BOJ adopts a formal inflation target without changing the current CPI methodology a lower band of less than 2 percent would not achieve its goal of price stability.