The decline in production was the largest since data for the present time series was first published in February 1953. As a result the ministry downgraded its output assessment to “declining rapidly.”

This report comes hot on the heels of an earlier one which showed that Japan’s exports plunged 26.7 percent in November, the sharpest drop since at least 1980. Japanese retail sales also fell in November -by an annual 0.9%. According to data from the Ministry of Economy, Trade and Industry, on a monthly, seasonally adjusted basis, sales were down 0.1% in November. Sales at large retailers decreased 3.2% on the year. These results were rather better than expected, but I wouldn't hold out much hope simply on that count, since the job market is still holding up reasonably well at this point, and consumers will be getting some benefit from slowing price increases (or even from price decreases) - and remember this data is not price corrected, which makes it all just a little bit misleading.

An Economy Trying But Failing To Generate Inflation?

Japanese consumer inflation declined in November, with the annual inflation rate falling to 1.0% (from 1.7% in October) on the general index. The index excluding fresh food also fell, from 1.9% to 1.0%. While the "core" core index - excluding fresh food and energy - came in at a stationary zero percent, down from October's 0.2% increase. In all three cases month on month inflation was negative.

Estimated headline inflation Tokyo in December (which is often thought to give an indication of future national trends) was down to 0.7% year-on-year (compared to 1.1% in November). Thus all the signs are there that Japan will soon be heading back into outright deflation, and the situation is only likely to get worse as the recession proceeds. Which brings us back to the inevitable question, was the BoJ right to bring quantitative easing to an end in 2006?

In fairness to the BoJ, they may well have been succumbing to pressure from other central bankers at the G7 level rather than making their own mistake here, since Japan's zero interest rates were perceived as a serious impediment to intriducing generalised monetary tightening against what was perceived to be a global asset bubble. The asset bubble undoubtedly existed, but it is not clear that Japan was at the root of the problem.

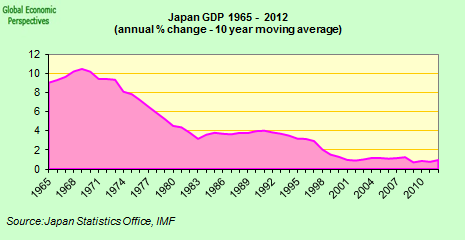

Paul Krugman once described Japan's economy as struggling to create inflation but being systematically incapable of doing so due to the presence of a liquidity trap - rather like a drowning man gasping for air who has the energy simply to bob up and down in the water, but not to swim to safety. As we can see in the chart below, "core" core inflation only barely broke the surface in what has been the longest boom in the Japanese economy since the start of the 16 "difficult years" in 1992. Food and energy prices certainly took off, but as these now come plunging down again, the negative shock will certainly send the "core" core diving after it and into negative territory - a Captain Ahab and the Moby Dick inflation dynamic, perhaps, with the BoJ playing the part of Ahab to Krugman's Ishmael.

In fact Krugman was advocating the bank commit to substantial inflation (he suggests 4%) over a long period of time (15 years) as a way of stirring up strong inflation expectations and this was really just to much for the Bank.

In fact Krugman was advocating the bank commit to substantial inflation (he suggests 4%) over a long period of time (15 years) as a way of stirring up strong inflation expectations and this was really just to much for the Bank.Many people apparently read my previous note as saying simply that Japan should print money like crazy. I have indeed said this in the past (see What is wrong with Japan? ), and see no harm in such a policy. But I now believe, based on the analysis in Japan's trap, that even a very large current monetary expansion will probably be ineffective. What is needed is a credible commitment to future monetary expansion, so as to generate expectations of inflation.How might the Bank of Japan achieve such a commitment? The natural way is to announce a target rate of inflation over the long term, with the announced intention of doing whatever is necessary to achieve that rate - basically the same as the inflation targeting now followed in, say, New Zealand or the UK, but with the objective being an inflation rate that is acceptably high rather than acceptably low The obvious question is how high a rate is needed, for how long. And the short answer is that I don't know, but I am working on it. A guess is that the required inflation rate isn't very high, but that people must expect it to last for a quite long time - we might for example be talking about, say, 4 percent inflation for 15 years..Japan's economy, yearning for inflation. Maybe Leonard Cohen had it right:

Paul Krugman - Musings and experiments surrounding Japan's Recession

Like a bird on the wire,

Like a drunk in a midnight choir

I have tried in my way to be free.

Leonard Cohen

Unemployment On The Rise As Job Market Tightens

Other data out this week show evidence of labour market tightening, and rising unemployemnt. There were 76 job vacancies open for every 100 applicants ratio in November, down from 80 in October, while the number of new job offers fell 23.7 percent in November from a year earlier and the jobless rate rose 3.9 percent in November from 3.7 percent in October. However we are still a long way from a significant rise in unemployment at this point, despite the fact that the evidence is growing that temporary and part-time workers - whose numbers have grown substantially in Japan in recent years - are increasingly being laid off. Japanese companies plan to fire around 85,000 of these workers by the end of the financial year, more than double the 30,067 forecast last month, according to data this week from the Labor Ministry. Undoubtedly that little line which has started to move upwards in the chart below will continue to do so in the months to come.

And Japanese real wages fell again in November - by 3.1% - making for the seventh consecutive month of decline.

And Japanese real wages fell again in November - by 3.1% - making for the seventh consecutive month of decline.

And to wind up this short, end of year data report, overall household spending was also down in November by 0.5% from a year earlier (in price-adjusted real terms) - the ninth consecutive month where spending has fallen. Spending by wage earners' households was up 1.2 percent in November from the same month a year ago. Wage earners' total cash earnings fell 1.9 percent in November from a year earlier, the first drop in nearly a year.