By Claus Vistesen: Copenhagen

As the discourse is slowly but surely tilting towards exit strategies, by part of central banks, from ultra low interest rates and unconventional measures the BOJ opted to day to maintain a very cautious stance towards the incoming green shoots and whether they will prove enough to lift Japan out of the mire.

(quote: Bloomberg)

Officials kept the benchmark overnight lending rate at 0.1 percent, and maintained their emergency lending programs to banks and companies. While describing the economy as “showing signs of recovery,” an upgrade from the “stopped worsening” assessment last month, the Bank of Japan said in a statement in Tokyo today that it still sees “downside” risks to growth. Today’s statement reflected global doubts about the strength of a recovery from the deepest recession since the Great Depression. A Bloomberg News poll of U.S. households published today showed Americans plan to refrain from boosting spending even after the biggest drop in consumption in 29 years.

“Most countries are experiencing a recovery, but few can be confident about the sustainability of those recoveries,” said Yoshiki Shinke, a senior economist at Dai-Ichi Research Life Institute in Tokyo. “Japan will be the last country to raise its interest rate” because it has the added problem of deflation, he said. Bank of Japan Governor Masaaki Shirakawa told reporters in Tokyo today that while stimulus measures have helped the economy improve, “we’re not confident about the strength of private final demand after those effects fade.” He added that central bankers are monitoring the appreciating exchange rate, which is contributing to the drop in Japanese consumer prices.

Japan's problems are many fold but the most severe issues in the context of reading the tea-leaves of the recovery is the uncertainty attached to question of whether the current above par environment will linger beyond the last effects of the stimulus (which was front loaded due to the elections) as well as any inventory bounce which may come as Japanese companies rebuild their empty shelves in Q3.

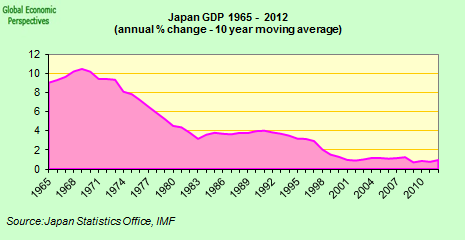

It is difficult not to sympathize with the BOJ in its careful approach here since if you take a look at the underlying demand conditions they are, to put it mildly, sluggish! Only a week ago, I discussed the situation on the corporate level where companies were hit by falling top line sales on the domestic market and, as a result, only very carefully expanding capex. Moving on to other key economic indicators it is pretty poor reading if we look at the domestic economy in isolation.

By far, the most preoccupying problem has to be the fact that Japan's inflation rate is moving beyond sub-zero and essentially into the abyss which is a painful and almost, if you will allow me to be dramatic, tragic outcome after two decades of fight against this very malaise. Now, I know that we are observing one-off effects from high oil prices in the summer of 2008, but try to have a look a the actual numbers. Consequently the index that actually includes energy is currently running (inJuly ) at a rate of decline of 2.2% whereas the index which excludes energy and fresh food is running at an annual decline of 2.6% and thus more than the headline gauge. Clearly, the BOJ would like to see this figure correct or even stabilize over the summer before contemplating tweaking nominal interest rates.

With respect to consumption, the figure tracked as a headline gauge for domestic demand on the consumer side is quite volatile, but it should not escape our attention that despite its volatility, it has been consistent below the 0% growth mark throughout 2009. Thus the average annual growth rate on a monthly basis has been -1.8% so far in 2008 which suggests as a simple yardstick the negative drift we need to apply to the evolution of domestic demand in Japan.

Finally there is the labour market where the unemployment rate has increased rather harshly since the beginning of 2009 following a mean reverting pattern around 4% throughout 2008. 5.7% which was the reading in July certainly won't make any headlines comparing to the eye-popping figure we are seeing in e.g. Spain or elsewhere, but it is worthwhile contemplating this in a relative sense and thus the effect it is likely to have on the behaviour of already cautious households.

Where Goes the JPY?

If the round-up above suggest, in a real economic context, the current shaky condition of the Japanese economy it seems that Japan now has a new issue to deal with; the unduly appreciation of the JPY. Now, of course these days it may be of less use to look at the JPY measured against G7 currencies rather than for example against China, but the graph below should still capture much of the essence.

I think it is very interesting here to observe that in a post-crisis context the JPY has gained about 20% against the Euro and Buck where it has been ranging since the latter part of 2008. Clearly, this has an effect on the real economy in so far as it reduces the competitiveness of Japanese companies relative companies in the US and Eurozone (not to mention the UK); and remember, deflation here is becoming a zero sum game since at the moment the US, the Eurozone, and the UK is also suffering from a bout of deflation or very low inflation.

Of course, this presents Japan with a whole new problem in the sense that while Japan could hitherto expect to get a double boost from an increase in risk aversion as carry trade activity took hold lowering the Yen and allowing Japan to export away, this route is gettingincreasingly crowded. More specifically, Bernanke has entered the scene and as analysts and commentators start talking about the new "victims" of the global carry trade punt in the form of those brave souls among central bankers who dare raise interest rates before movement in the G3, Japan cannot be certain to be the exclusive funding currency. It has a rival in the form of the USD and notwithstanding the obvious consequences for the global economy that Bernanke is putting up a 0% interest rate on the world's most liquid fiat instrument, Japan might find itself pinched here.

Of course, there is a solution here even though it seems unlikely at the moment, I believe, that it will come to pass.

It was still telling that the branch of RBS in Japan (RBS Securities Japan Ltd) was quoted, by Bloomberg yesterday, personified by chief economist Junko Nishioka for noting, rather dryly I'd might add, that the most efficient way to spur growth in Japan would be through a devaluation. Hmm, that would be fun wouldn't ... a devaluation amongst the G3! Once again, we are left guessing as to just what value of the benchmark USD/JPY that will jolt the MOF and BOJ into joint action; 90, 85, 80, 75 ...? I will leave my readers to do the rest of the guesswork, especially since yours truly has burnt his prediction powers once too many trying to call JPY intervention. So far though, most bets seem off as the incoming Finance Minister Hirohisa Fujii made it quite clear that there will no such nonsense of intervention to weaken the Yen. Also, if Macro Man is right and this is predominantly a Dollar story rather than a Yen story, then what can they do as MM put it earlier this week.

In a general sense, it shall be most interesting to following both intra G3 currency movements and FX in general if and when some economies venture into a decisive tightening mode over the second half of 2009. And for Japan, well she will try to muddle through of course. I am watching the inflation picture closely as well as of course we must watch the extent to which Japan can really couple on to the Asian growth spurt we are currently observing. With respect to policy decisions, I feel confident that the BOJ is locked in at this point to, if not continue QE, then at least to keep nominal interest rates at or very close to the zero bound.

---

[1]: Note, if you correct for stationarity the co-relationship dissipates so I may be over-stepping my bounds here.